What Happens When Supply Falls 26% and Demand Refuses to Follow

Market Update Nick Granoski July 15, 2026

Market Update Nick Granoski July 15, 2026

Quick Take:

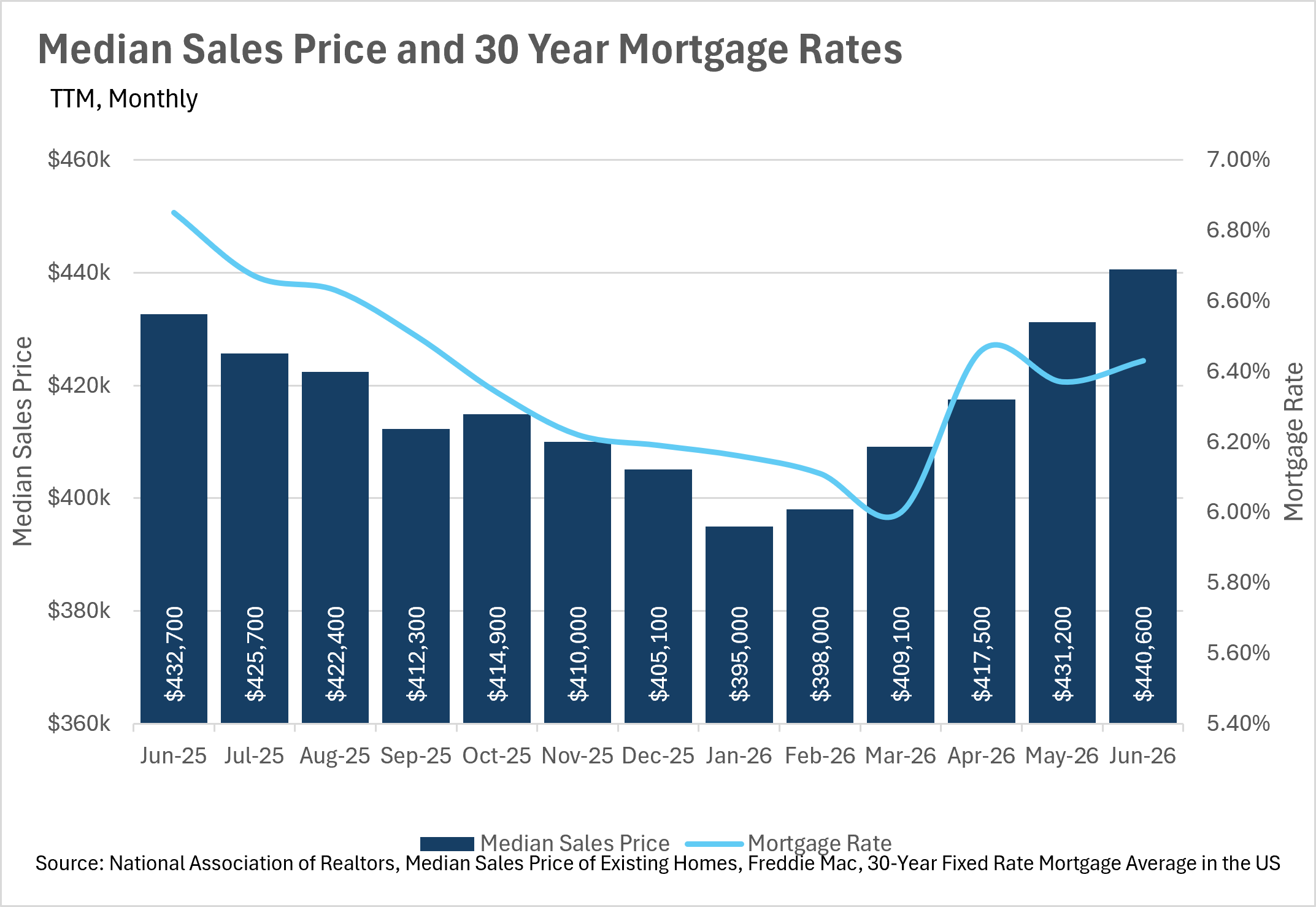

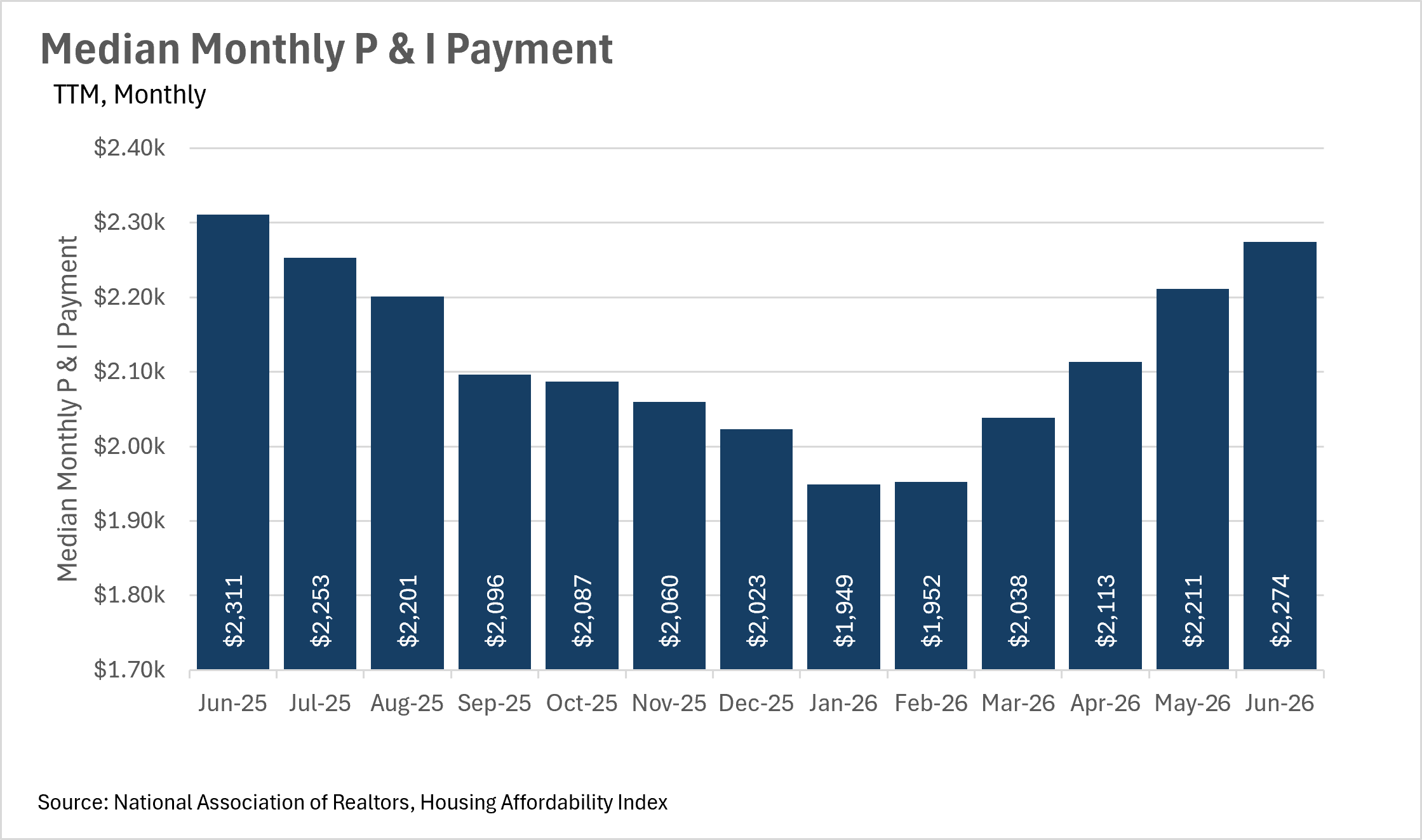

The spring rally that began back in January has officially pushed median home sale prices to their highest level in a year. In June, the median home sold for $440,600, representing a 2.18% month-over-month increase and a 1.83% year-over-year gain. This marks the fifth consecutive month of month-over-month price increases, and the median sale price has now surpassed the $432,700 peak we saw in June of last year. However, the affordability picture isn't quite as rosy as it was earlier in the year. Mortgage rates ticked up slightly to 6.43% in June, and the combination of rising prices and rates that have bounced off their March lows has pushed the median monthly P&I payment up to $2,274. While that's still 1.60% lower than the $2,311 the median homeowner was paying a year ago, the gap is shrinking fast. Back in January, the median P&I payment was $1,949, so monthly payments have risen by more than $300 in just five months. If this trend continues, the affordability gains that lower rates provided earlier in the year could be fully erased by the end of the summer.

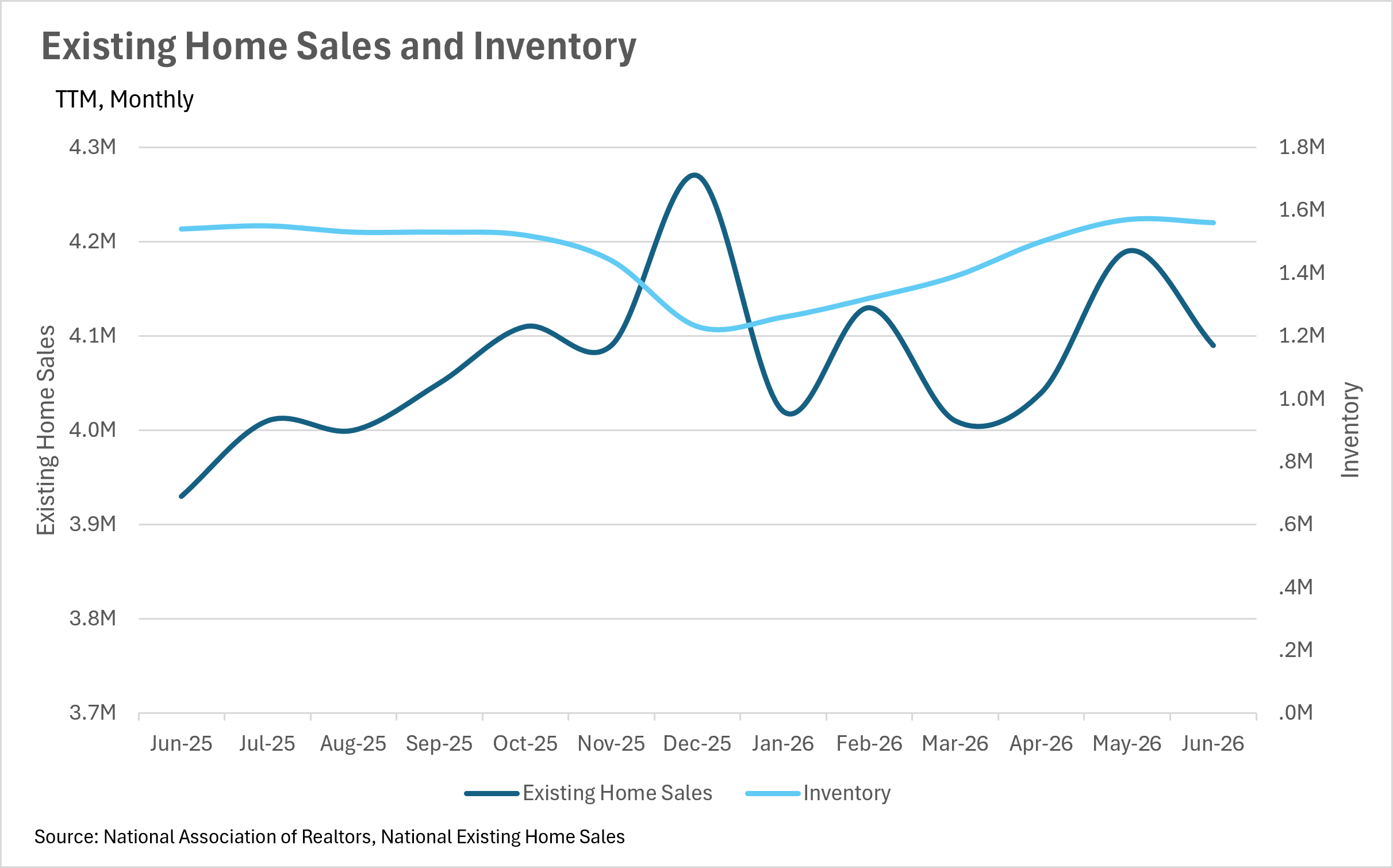

After climbing steadily from the December low of 1,230,000, inventory levels appear to have plateaued. In June, there were 1,560,000 homes available for sale, representing a slight 0.64% month-over-month decline from the 1,570,000 we saw in May, though still 1.30% higher than where we were at this time last year. On the new listings front, 463,480 new listings hit the market in June, representing a 2.45% year-over-year increase but a 2.42% month-over-month decline from May. This pullback in both inventory and new listings could signal that the spring surge of supply is beginning to taper off, which would be notable given that June and July are typically peak months for inventory. If inventory begins to decline further while demand remains strong, we could see the market tighten up heading into the back half of the summer. On the other hand, inventory levels are still roughly in line with where they were last year, so there's no reason to panic just yet.

Existing home sales came in at 4,090,000 in June, representing a 4.07% year-over-year increase, the strongest year-over-year gain we've seen in quite some time. That said, sales did pull back by 2.39% from May's pace, which isn't unusual given the typical seasonality of the market. The year-over-year increase is the real headline here, as it tells us that buyers are meaningfully more active than they were at this point last year. This is likely being driven by a combination of factors: mortgage rates are still lower than they were a year ago, inventory is providing more options to choose from, and the steady march of price appreciation may be creating a sense of urgency among buyers who don't want to wait any longer. The question heading into the second half of the year is whether this momentum can be sustained. With mortgage rates hovering in the mid-6% range and monthly payments creeping higher, we could see some buyers pull back if affordability continues to erode.

When determining whether a market is a buyers' market or a sellers' market, we look to the Months of Supply Inventory (MSI) metric. The state of California has historically averaged around three months of MSI, so any area with at or around three months of MSI is considered a balanced market. Any market that has lower than three months of MSI is considered a seller's market, whereas markets with more than three months of MSI are considered buyers' markets.

Right now, the national market appears to be tilting in favor of sellers. Existing home sales are up more than 4% year-over-year, which means demand is absorbing the available supply at a healthy clip. At the same time, inventory has plateaued and even declined slightly on a month-over-month basis, which means the supply side of the equation isn't growing fast enough to offset the increase in demand. If this dynamic persists through the summer, we could see months of supply tighten further, giving sellers even more leverage. However, with monthly P&I payments rapidly approaching where they were a year ago, there's a chance that demand cools off in the coming months, which would bring the market back toward balance. As always, real estate is a highly localized asset, which is why you should check out what's going on in your local market below in the Local Lowdown!

Quick Take:

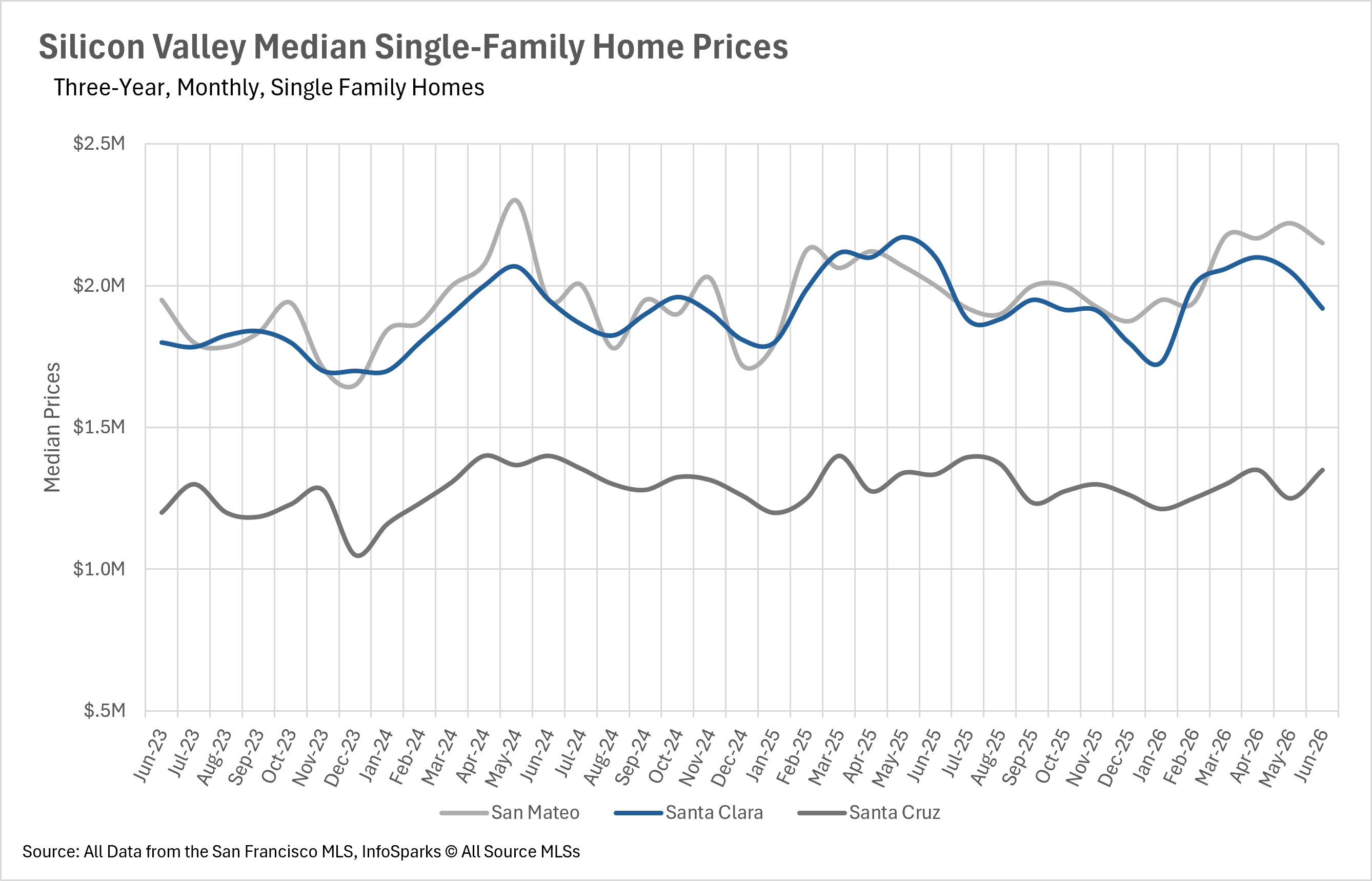

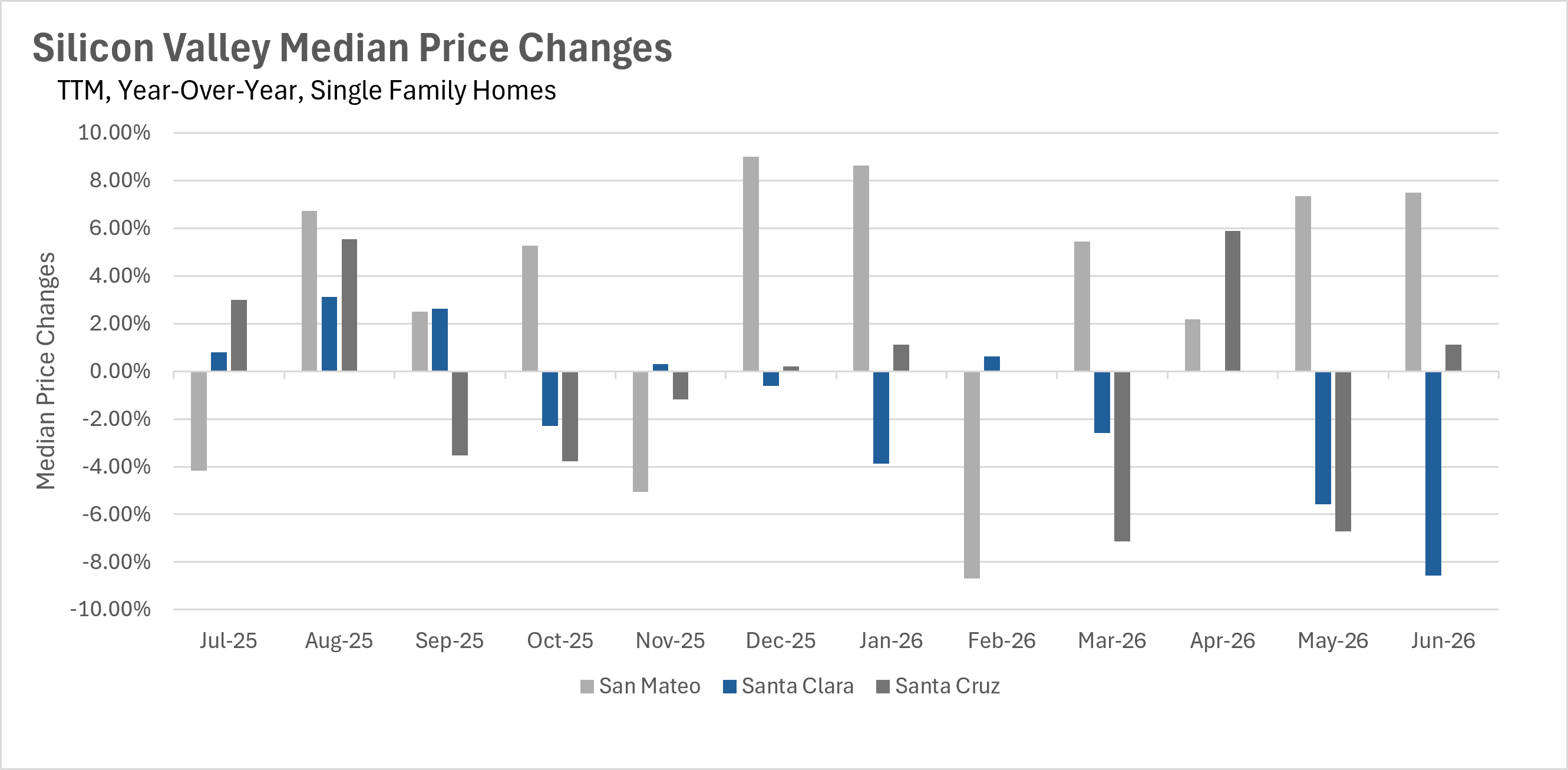

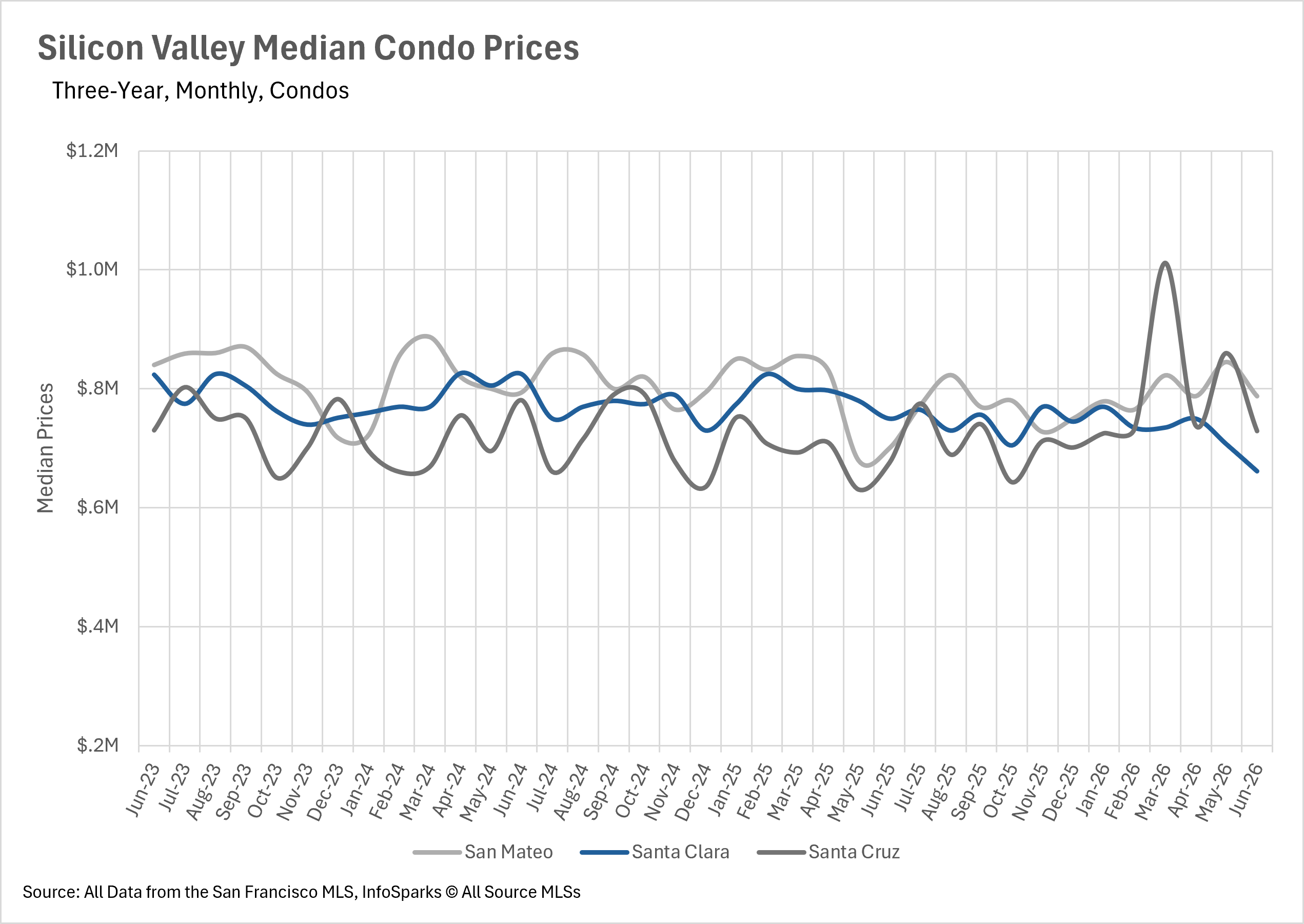

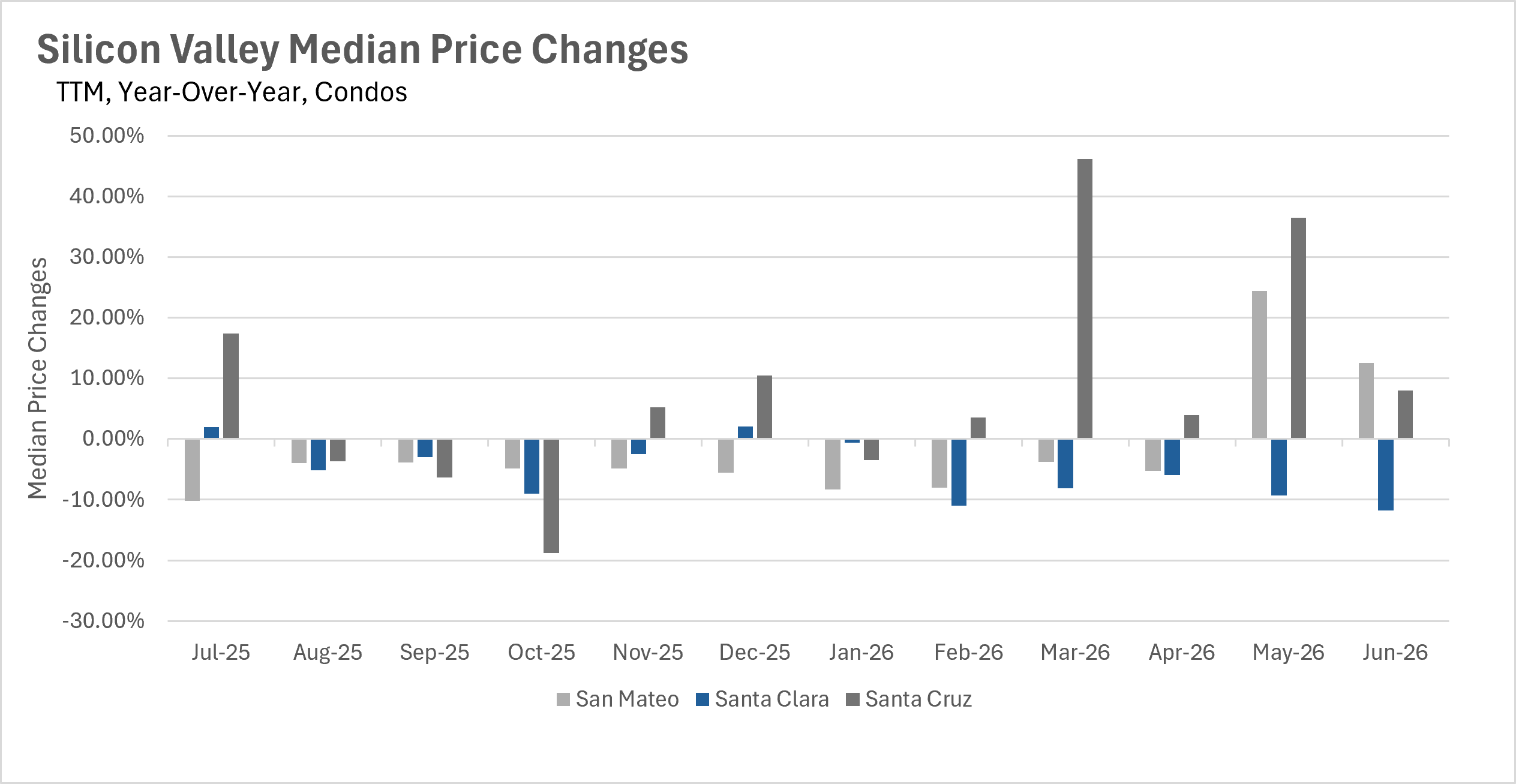

The single-family home market in Silicon Valley showed divergent trends in June as we move deeper into summer. San Mateo County posted an impressive 7.50% year-over-year increase in median sale price, with the median home selling for $2,150,000. Santa Cruz County also showed modest gains, with the median home selling for $1,350,000, representing a 1.12% year-over-year increase. However, Santa Clara County experienced a significant 8.57% year-over-year decline, with the median home selling for $1,920,000. The condo market painted a similar picture, with San Mateo County condos surging 12.50% year-over-year to $787,500 and Santa Cruz County condos climbing 7.96% to $728,750, while Santa Clara County condos dropped 11.80% to $661,500.

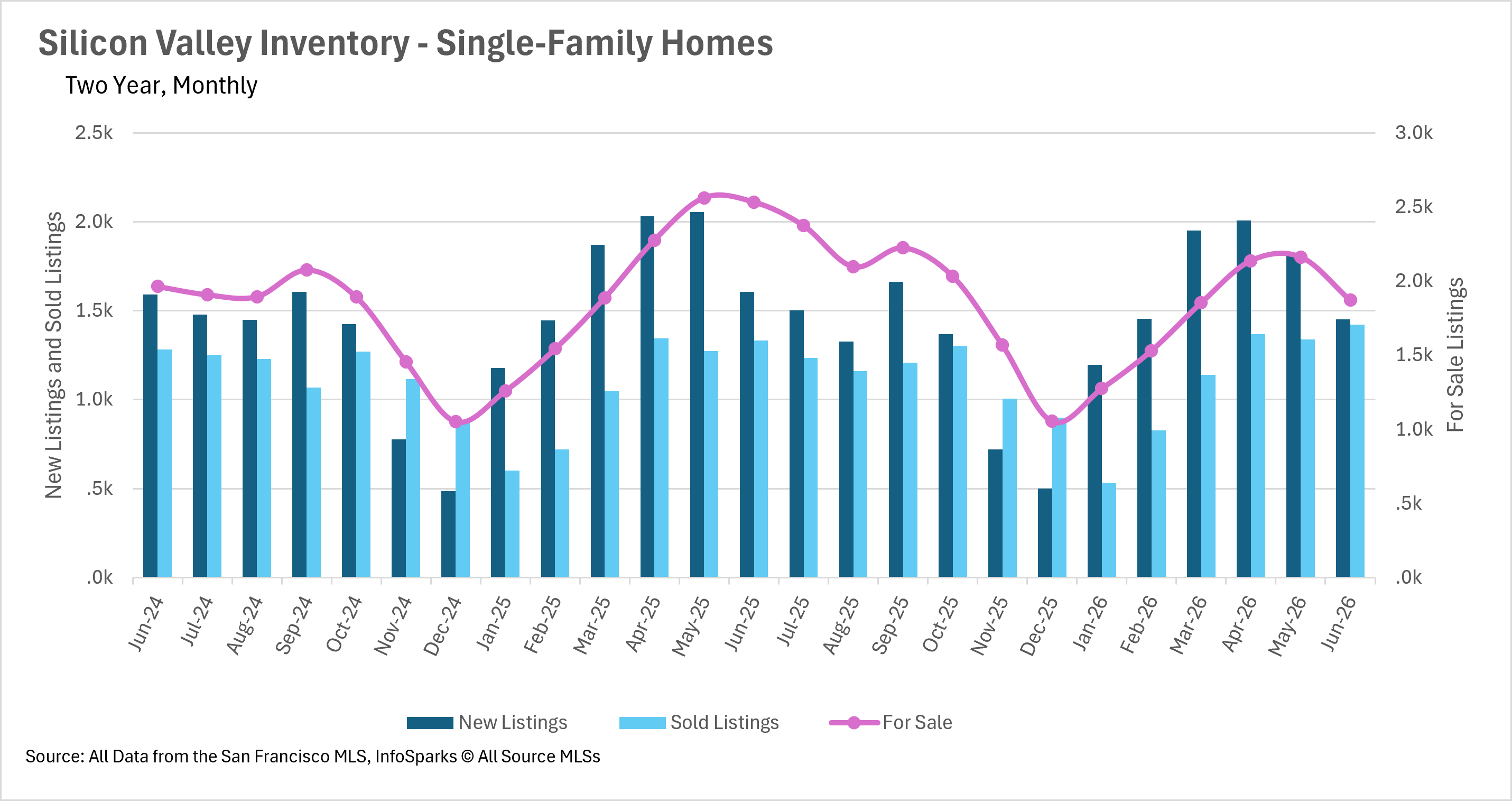

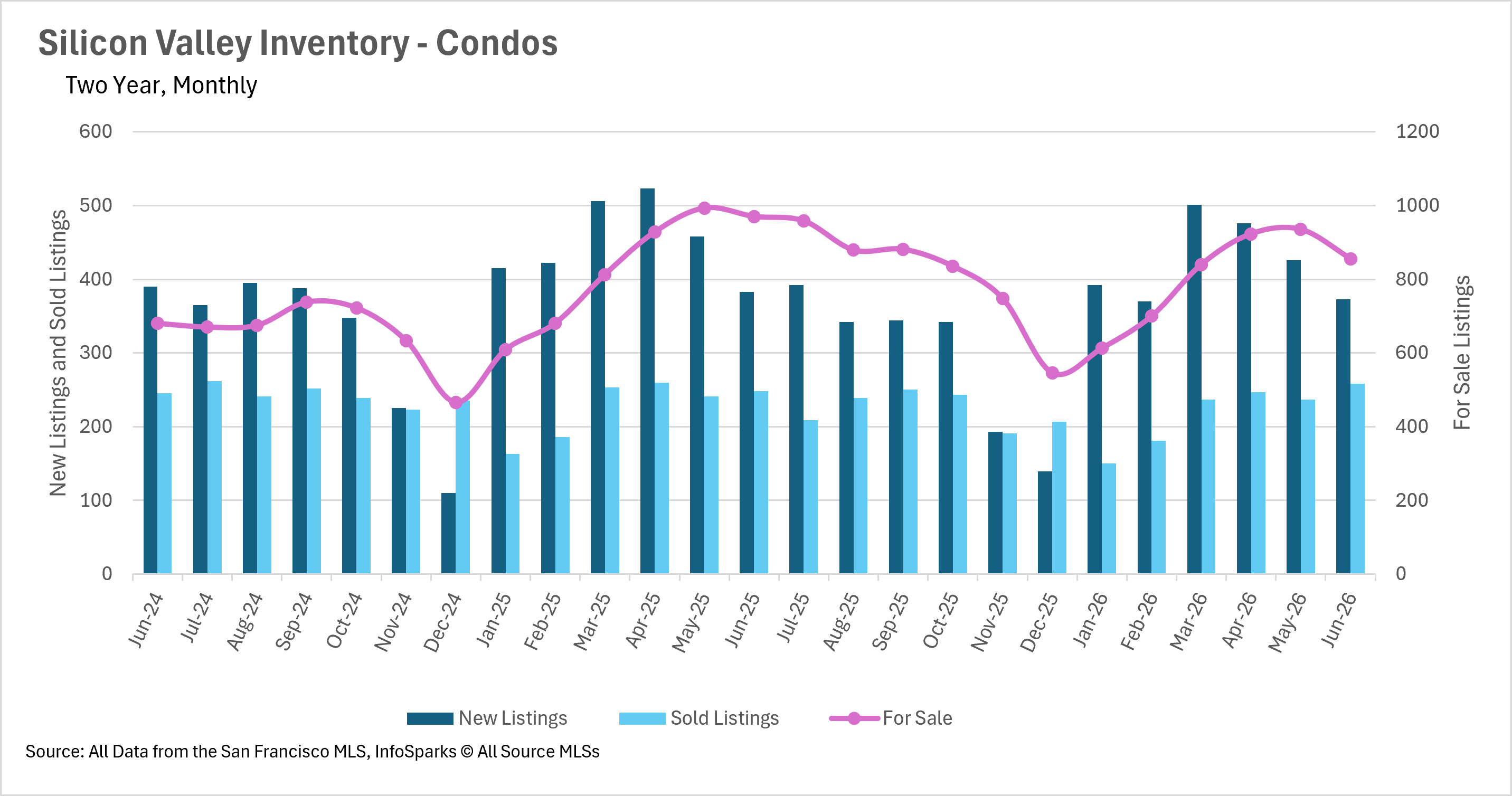

The inventory situation in Silicon Valley has become remarkably tight as we head into the heart of summer. There are currently just 1,870 single-family homes for sale across the region, representing a substantial 26.15% year-over-year decline. While new listings are down 9.59% compared to last year, sold listings jumped 6.91%, demonstrating that buyer demand is absorbing available inventory at an impressive pace. The condo market is experiencing similar constraints, with 856 condos currently for sale, down 11.75% year-over-year. This dramatic inventory shortage is creating fierce competition among buyers, particularly in the single-family home segment where options are increasingly limited.

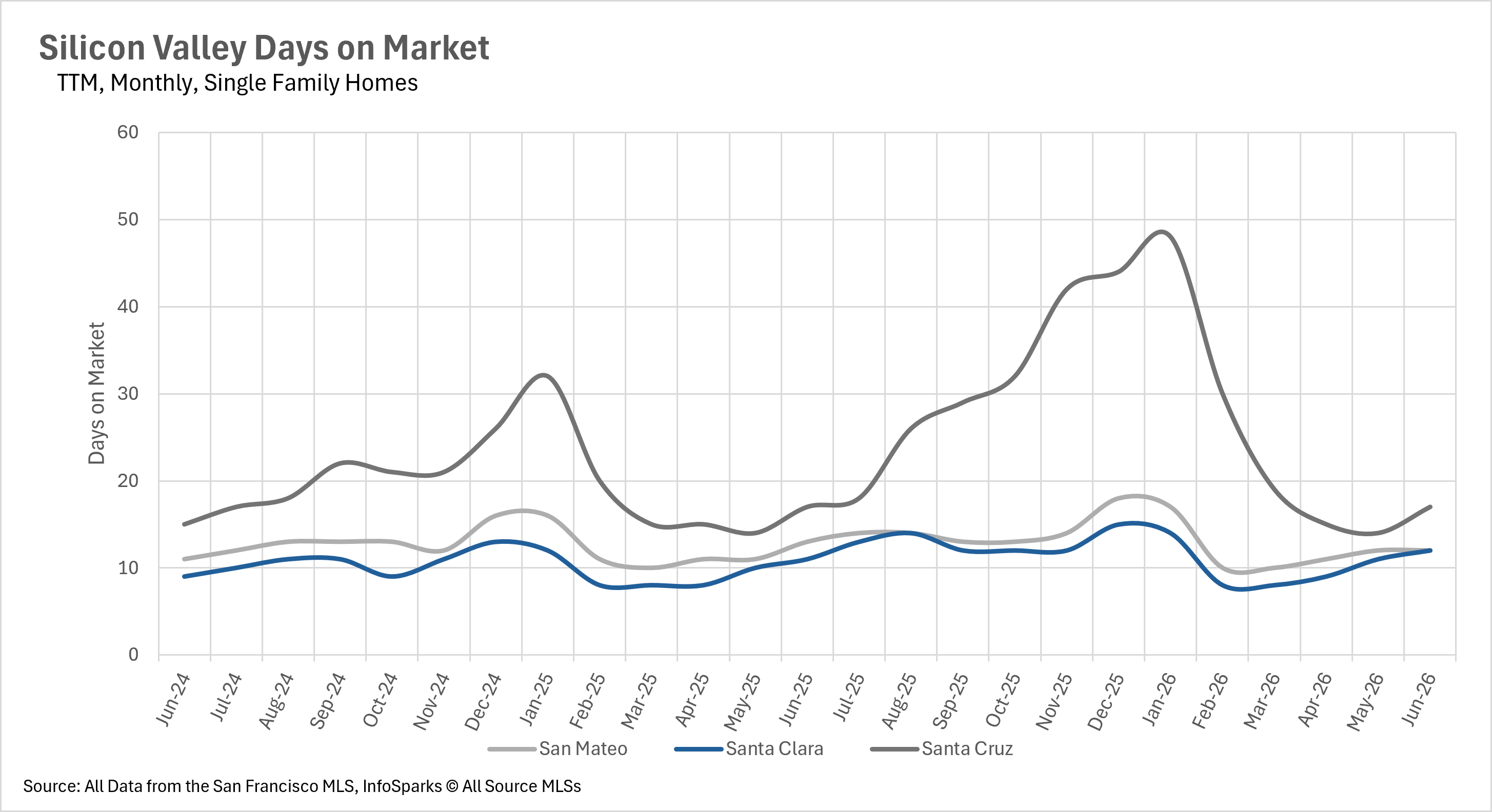

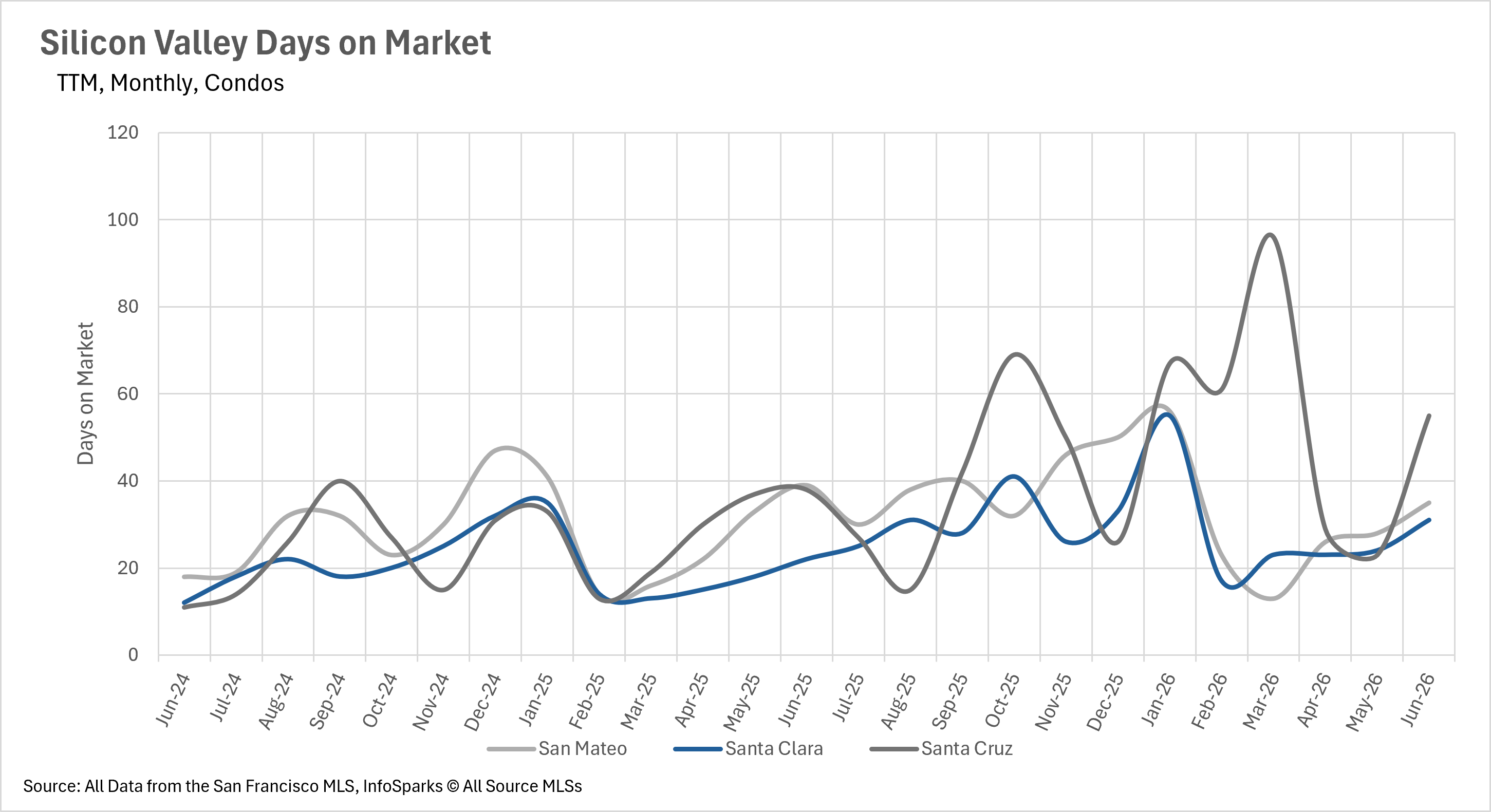

Single-family homes are selling at a blistering pace throughout Silicon Valley this summer. In San Mateo County, the average single-family home is selling in just 12 days, representing a 7.69% improvement compared to last year. Santa Clara County homes are also spending 12 days on the market, while Santa Cruz County homes are averaging 17 days, unchanged from this time last year. The condo market presents a more mixed picture. San Mateo County condos are selling 10.26% faster than last year at 35 days on average. However, Santa Clara and Santa Cruz County condos are taking considerably longer to sell, with year-over-year increases of 40.91% and 44.74%, bringing their average days on market to 31 and 55 days, respectively.

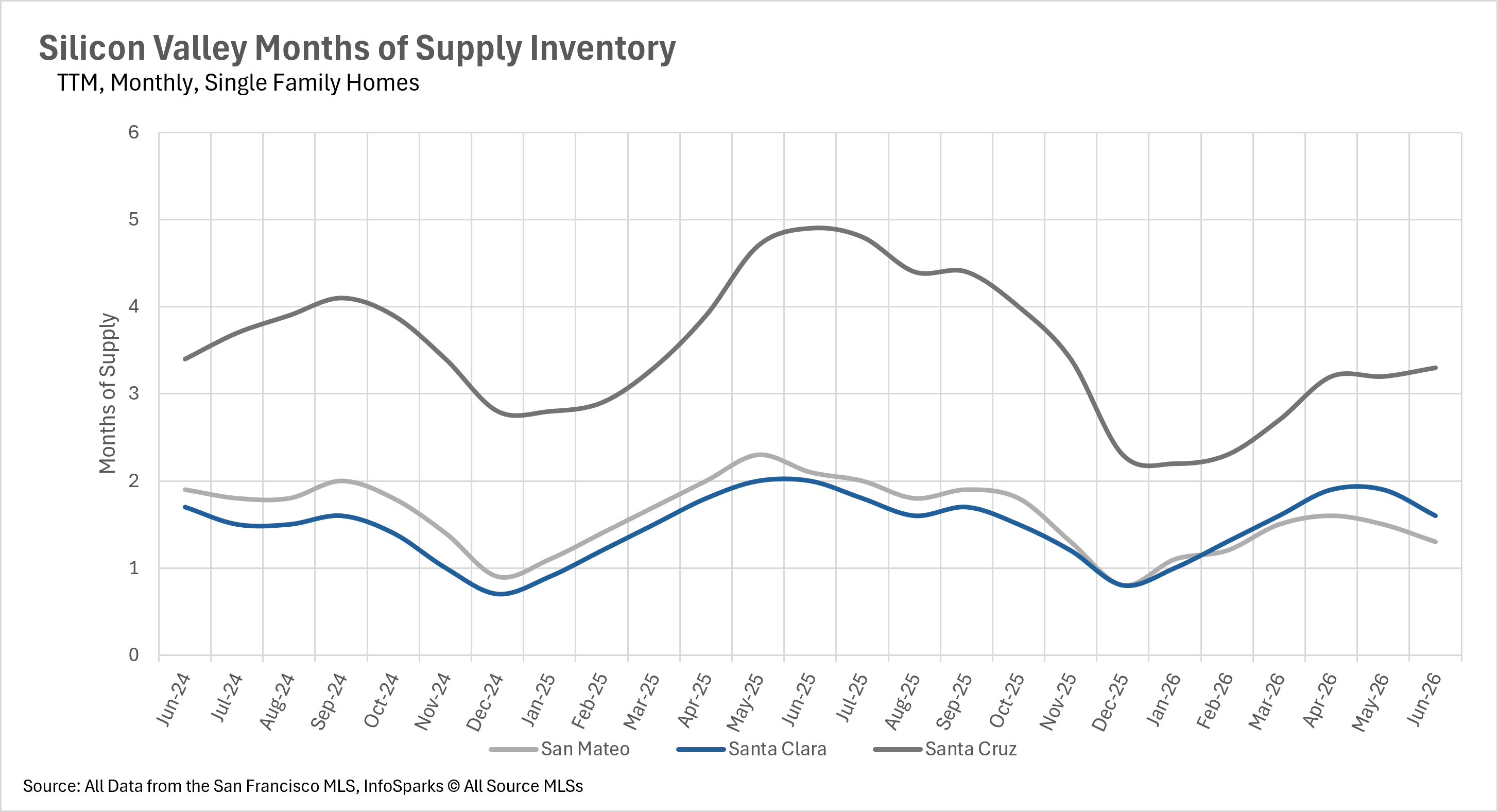

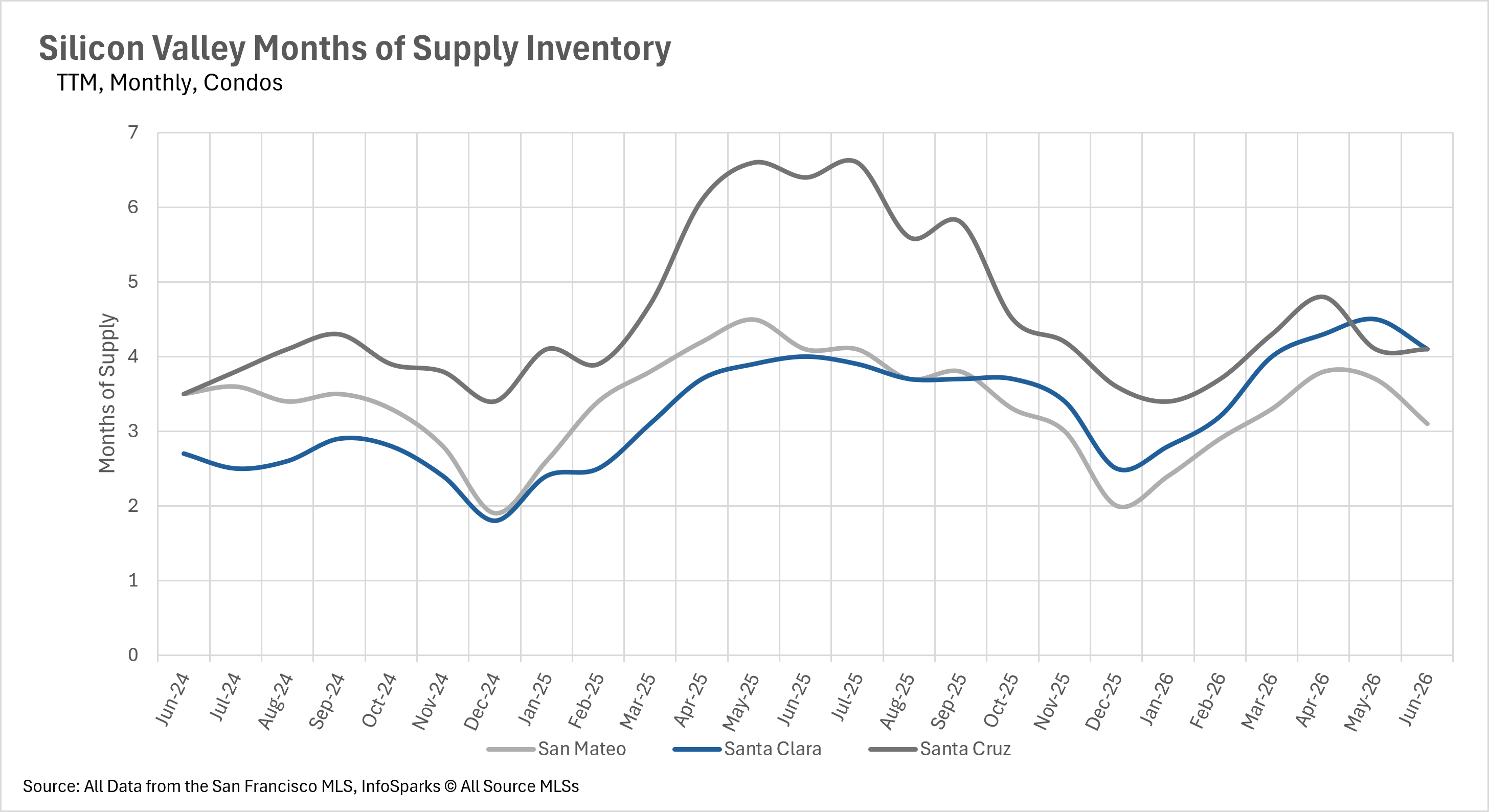

When determining whether a market is a buyers' market or a sellers' market, we look to the Months of Supply Inventory (MSI) metric. The state of California has historically averaged around three months of MSI, so any area with at or around three months of MSI is considered a balanced market. Any market that has lower than three months of MSI is considered a seller's market, whereas markets with more than three months of MSI are considered buyers' markets.

The single-family home market has become an even more pronounced seller's market compared to last year. San Mateo County has just 1.3 months of supply on the market, representing a dramatic 38.10% year-over-year decline. Santa Clara County has 1.6 months of supply, down 20% from last year, while Santa Cruz County has 3.3 months of supply, a substantial 32.65% year-over-year decrease that has brought it much closer to balanced market territory. The condo market is more favorable for buyers, with San Mateo County at 3.1 months of supply (down 24.39% YoY), and Santa Clara and Santa Cruz Counties both at 4.1 months. With single-family inventory at critically low levels and homes selling in under two weeks, buyers in that segment should be prepared for intense competition throughout the summer!

Stay up to date on the latest real estate trends.

Market Update

Real Estate 101 | Los Altos

Real Estate 101 | Woodside

Market Update

Real Estate 101 | Palo Alto

Real Estate 101 | Atherton

We know that real estate transactions can be complex, but with our expertise, they don’t have to be stressful. Our team is dedicated to handling every aspect of your Mid-Peninsula real estate needs with the utmost care and professionalism. From the initial consultation to the closing, we manage all the details so you can focus on your future. Whatever challenges arise, trust that we’ve got this — your success is our top priority.